ABOUT THE PRACTICE PERFORMANCE INDEX

The Practice Performance Index — a survey of more than 2,200 physicians and practice administrators — provides an annual window into the issues affecting the financial and operational health of physician practices across the US. It serves as a barometer of the current state of physician practices and provides insight into physician outlooks on the year ahead.

This year’s PPI focuses on what ‘High Performing’ practices are doing to adapt to the New Medical Economy (Access Full Report), with its focus on value-based care, the consumerization of medicine, new technology opportunities and changing business pressures. Our study found that those groups that embrace this new medical economy will be rewarded with higher growth, a more loyal patient base and more satisfied providers.

THE QUALITIES OF HIGH PERFORMING PRACTICES

Has implemented or will soon implement plans for the new value-based care reimbursement models.

Drives key practice performance indicators through the adoption of new technologies

Focuses on improving

the patient experience through new technologies and better services

Collects regular feedback from patients through a variety of touch points, including online reviews

CHANGING

REIMBURSEMENT MODELS

Uncertainty and slow responses to address value-based care

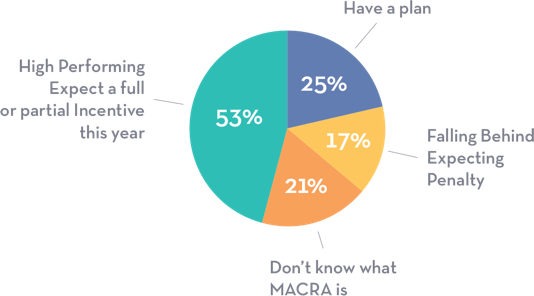

Medical practices across the US have been slow to react to changes in the way insurance markets and reimbursement models. Only a quarter are acting on a plan, with a further 20% waiting to put their plan into action. There is a clear link between high performance and proactivity when it comes to regulatory changes in the marketplace: while 56% of ‘High Performing’ practices have a plan, only 34% of ‘Falling Behind’ ones do.

INNOVATIONS IN HEALTHCARE

Technology adopters are seeing improved practice performance outcomes

The PPI reveals that ‘High Performing’ medical groups are more likely to realize that new technology has the potential to improve the quality of care they provide, not just improve efficiency or productivity. This different attitude toward technology results in higher use of new technologies, including patient portals, advanced analytics for population health management, telemedicine and iPad-based intake forms.

‘High Performers’ are twice as likely to adopt new technologies that differentiate them and deliver choice to patients.

PATIENT EXPERIENCE IMPROVEMENTS

Patients are demanding more from their healthcare experience

As patients increasingly face higher deductibles, co-pays and co-insurance, their decision-making is dramatically changing. They bring the high expectations and stringent requirements from other areas of their life to their healthcare experiences, in part because there is more choice than ever on how to get care and because new technologies are making it easier to compare providers.

This year’s findings demonstrate that the most successful practices are offering more same-day appointment times and are implementing new technologies such as telemedicine, check-in kiosks and expanded payment options and plans. Collecting feedback and online reviews also helps distinguish high performing practices.

INCREASED COMPETITION IS HERE TO STAY

Intensified competitive pressure and a wave of consolidation are compounding pressures

Close to half of all practices have experienced intensified competitive pressure over the last three years, with signs that these pressures will intensify over the coming three years. The healthcare landscape is changing – there is no longer any question about it – and for medical groups that want to not just cope, but thrive, the path ahead is clear. What is encouraging is that the actions that practices should take to be high performers are likely to pay dividends across all areas of performance: proactivity, openness, and a patient-centric approach to investments.

Get Full Report Now